Understanding French Tax: What is the Revenu Fiscal de Référence?

Essential Reading

For French residents, your annual tax notice or avis d’imposition is a crucial document that not only informs you of your income tax liabilities but serves as proof of your taxable income and revenu fiscal. But what exactly do all those different totals mean, and why is the revenu fiscal de référence so important? Here’s what you need to know.

Your Avis d’imposition

Everyone who is tax resident in France (along with some French second-home owners) will need to file an annual tax return in France, and will consequently receive an ‘avis d’imposition’ or tax notice. These are typically made available in your online tax account from late July through August and will detail your annual revenue, taxable income, and any taxes owed.

But your avis d’imposition (also referred to informally as an avis d’impôts) isn’t simply a tax bill. It’s also one of the most important documents you will be issued in France and serves as your official proof of income. You will likely be asked for your avis d’impôts during any legal, financial, or tax procedure in France, for example: renting an apartment or applying for a mortgage, applying for or renewing your carte de séjour or residency card, taking out a loan, or applying for benefits.

You should be able to access all of your avis d’impositions via your online tax account, but it’s a good idea to print out a hard copy or save each one as a pdf to your computer for your records.

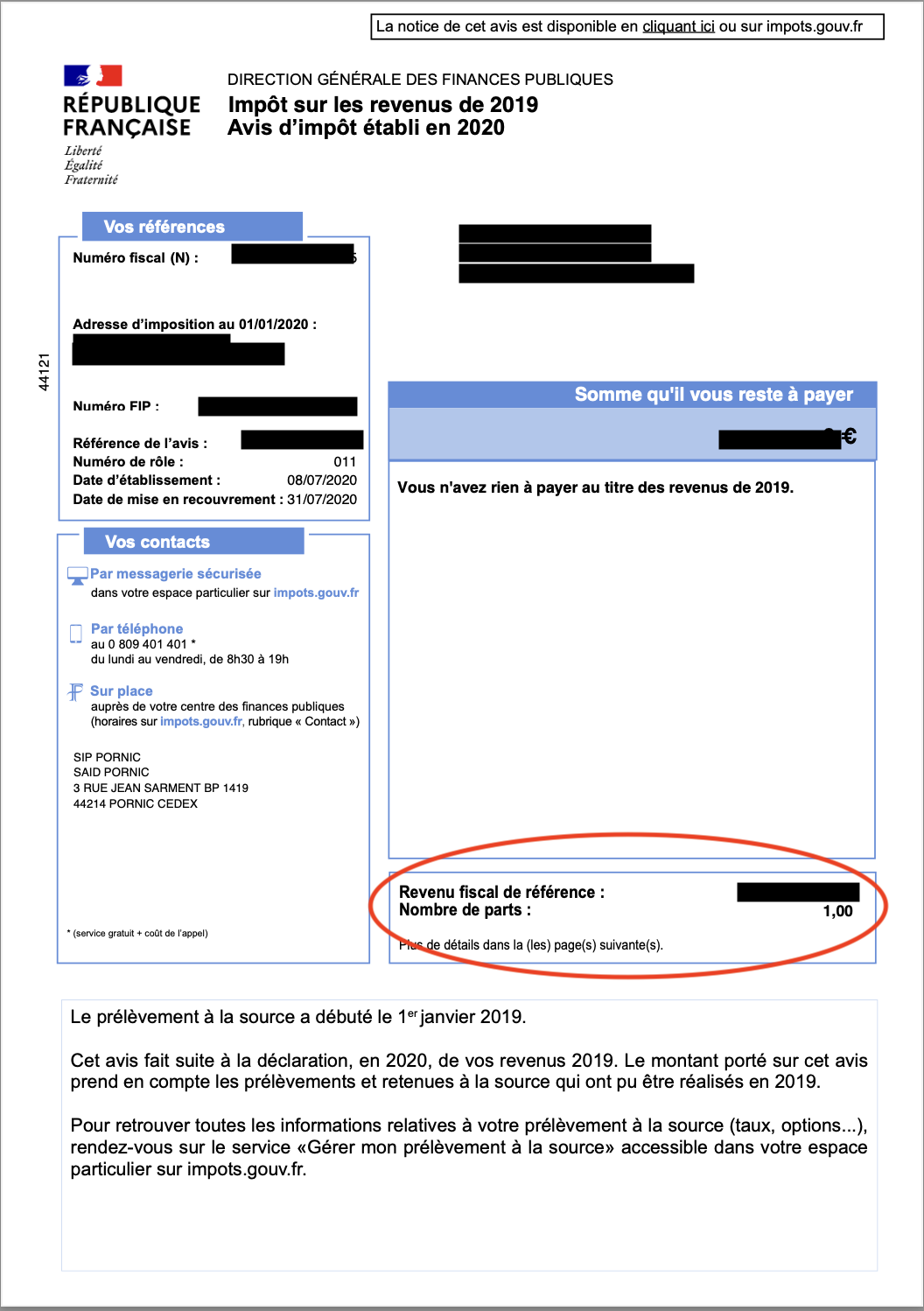

What is the ‘Revenu Fiscal de Référence’ on my French tax notice?

On the first page of your avis d’imposition, you’ll see two key figures:

- The ‘somme qu’il vous reste à payer’ – the amount of tax that you owe.

- The ‘revenu fiscal de référence’ – your household’s ‘reference tax income.’

So, what exactly is the revenu fiscal de référence? It’s a common mistake for expats to assume that this number refers to your household’s net taxable income (and in many cases, you may find that these two numbers are identical). However, that’s not actually the case. The revenu fiscal de référence takes into account the entirety of a household’s resources, including both the net taxable income and certain other tax-exempt income and deductible charges. It is calculated by the tax authorities based on the income you have declared, whether you are imposable (liable to tax) or non imposable (not liable).

Revenu fiscal de référence, revenu brut, revenu net : what’s the difference ?

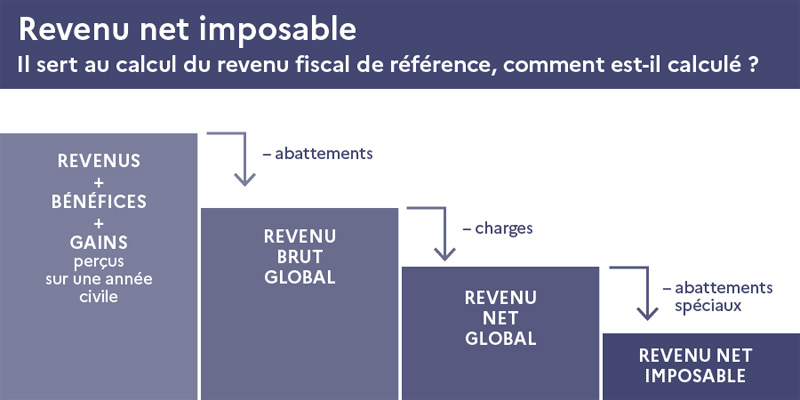

Let’s take a look at how the revenu fiscal de référence is calculated. Naturally, French tax is an incredibly complex subject, and if you want to fully understand all the charges, deductions, credits, and calculations that go into assessing your tax liabilities, we recommend seeking the advice of a qualified tax advisor. However, we’re going to simplify things for the sake of understanding and focus on the total figures you may see listed on your tax notice.

There are four main totals that you may see on your avis d’impôts, and they all refer to different calculations. Note that depending on your professional situation and revenue sources, you may not see all of these on your tax notice, but all tax notices will have a revenu fiscal de référence.

Revenu brut global

The “total gross income” refers to all of your income, profits, and gains received over the year, minus any abattements (tax-free allowances).

Revenu net global

The “total net income” refers to the total gross income minus any tax-deductible charges (expenses).

Revenu net imposable

The “taxable net income” refers to the total net income minus any abattements spéciaux (special allowances, typically reserved for those over 65, people with disabilities, and similar situations).

Revenu fiscal de référence

The “reference tax income” reflects the available resources of a household and is calculated by taking the revenu net imposable (taxable net income) and adding back certain items. These include:

- Certain tax-exempt income, such as certain tips or the remuneration of employees posted overseas

- Certain income subject to a prélèvement libératoire (flat-rate discharge levy), for example income from capitaux mobiliers (investment income)

- Certain deductible abattements (such as the 40% allowance on dividends)

- Certain charges deductible from income (such as épargne-retraite or retirement savings contributions deducted from your overall income)

- Taxable real estate capital gains (plus-values immobilières)

See the official guidelines here.

Image from economie.gouv.fr

Why is the revenu fiscal de référence important?

Your French tax notice serves as your official proof of income and resources in France, and the revenu fiscal de référence in particular is used to determine a wide range of rights, benefits, and obligations.

According to service-public.gouv.fr, the RFR is used in the following situations, among others:

- Tax exemptions and reductions: for example, whether you qualify for a taxe foncière exemption or reduction, or certain crédits d’impôt (tax credits)

- Social charges: the RFR determines which rate of CSG applies to your pension or other replacement income (0%, 3.8%, 6.6%, or 8.3%)

- Social assistance and benefits: including bourses des collèges (school grants), social housing applications, and CAF benefits

- Savings products: eligibility for a livret d’épargne populaire (LEP)

- Government grants: such as the bonus écologique for vehicle purchases and MaPrimeRénov’ for energy-efficient renovations

- Prélèvement à la source: determining whether a zero rate of income tax withholding applies to you

- High earners: the RFR is used to calculate the contribution exceptionnelle sur les hauts revenus (exceptional contribution on high incomes)

Note that in most cases, it is the RFR from your most recent avis d’imposition that is used. For example, the RFR calculated on your 2024 income (shown on your 2025 avis d’imposition) would be used for determining eligibility in 2026.

Paying Your Taxes in France

Whether you are moving to France, own French property, or have business interests, assets, or investments in France—FrenchEntrée is here to help with all your tax questions. Our Essential Reading articles are designed to give you an overview of the basics, from income tax and social charges to wealth tax and property taxes. However, tax laws and rates are always subject to change, and international tax liabilities can be especially complicated, so if in doubt, we always advise discussing your personal situation with one of our recommended financial or tax advisors.

Disclaimer: This guide is provided for general information purposes only and is not intended to be a substitute for professional advice regarding any aspect of your tax planning or tax liabilities in France. FrenchEntrée cannot be held responsible for the consequences of decisions or actions you may choose to take in connection with French tax declarations or tax liabilities.

Want more help with your France property journey? Join Membership, search our Property Portal, subscribe to French Property News, and follow our YouTube channel for the latest advice and updates. Join us at the French Property Exhibition for expert advice and property inspiration.

Lead photo credit : Shutterstock

Share to: Facebook Twitter LinkedIn Email

More in french tax, tax

Related Articles

By FrenchEntrée

Leave a reply

Your email address will not be published. Required fields are marked *